The Government of Canada has introduced the Underused Housing Tax Act (UHTA) which came into effect on January 1, 2022. The filing and payment obligations generally apply to non-resident non-Canadian owners residential property, but some Canadian owners are also subject to filing obligations.

The filing due date is April 30th of the next calendar year and note that this is an annual filing. Significant penalties are imposed for failing to file an annual return; minimum of $5,000 for individuals and $10,000 for corporations. It is worth repeating, these penalties are for failure to file the return; even if you think the property is not subject to the tax because it is occupied, you might still need to file.

The definition of “residential property” and “owner” are relatively straight forward and can be read about here. One area of this Act that can catch people off guard is the definition of “excluded owner” and “affected owner” which is what I want to focus on here because that will determine the filing obligations.

Excluded Owner

Since I am writing for individuals and small business owners, I will only address the excluded owner definitions most relevant to you (hopefully). For details check out the other links in this post or contact us directly.

Excluded owners do not have to file or pay any taxes under the Act.

Canadian citizens and permanent residents are excluded owners unless they are the owner of residential property as either:

a trustee of a trust (except if you are the personal representative of a deceased individual, in which case you are an excluded owner of the residential property)

a partner of a partnership

One important group that is not excluded are private corporation holding residential property. This means holding companies owning residential real estate (ie. for the purpose of asset protection, financing, etc), will be required to file even if they are ultimately not liable for any tax under the Act. This means that whether the private corporation is owned by Canadians or not, it must file a return.

Affected Owners

Affected owners, as the name implies, is everyone affected by the Act which means all affected owners must at least file a return, and may potentially be required to pay the Underused Housing Tax.

The CRA defines affected owners as everyone who is not an “excluded owner” in the definition above. Some important examples of affected owners include:

Individuals who are not citizens or permanent residents of Canada

Canadian citizens and PR who are either acting as a trustee (other than as a personal representative of a deceased individual) or as a partner of a partnership

Note that the immigration status of the beneficiary or partner is not relevant, the affected owner must still file if everyone involved is Canadian or PR.

Private corporations whether Canadian or not.

March 27th 2023 Update

On March 27th 2023, the CRA announced that they would provide administrative relief for the 2022 tax year. The due date for the 2022 tax year is still May 1st 2023 but no penalties or interest will apply for UHT returns and payments that the CRA receives by October 31st 2023.

The new anti-flipping measure took effect in January 2023 and is another effort by the government to control real estate speculation in Canada, similar to the foreign buyer ban. If real estate is bought and sold within 365 days, the CRA deems the property to be “flipped property” and any profit from the transaction is treated as business income to the taxpayer. There are specific exemptions outlined below.

The anti-flipping measure was put into place by Bill C-32 and amends the Income Tax Act (the “ITA“) to add a subsection specifically to deem proceeds from a “flipped property” as business income meaning 100% of the profit is included as income for the taxpayer. In the past, one of the advantages of transacting in real estate was that the profit could be treated as a capital gain and therefore only 50% of the profit would be taxed in the hands of the taxpayer.

Even before this anti-flipping measure, if a taxpayer flipped property, it would still generally be classified as business income. But taxpayers who did this in their personal capacity often reported any profits as a capital gain by justifying the real estate as an investment property and/or making use of the Principal Residence Exemption (more on that below). The new anti-flipping measure introduces a “bright-line rule” to prevent taxpayers from taking advantage of this grey area.

What is “Flipped Property”?

It is important to distinguish between the colloquial term we use everyday when we talk about “flipping property” and the CRA definition.

Colloquially, a simple definition of flipping property is the act of buying and selling a property quickly for profit.

In the anti-flipping measure, the CRA’s definition of “flipped property”: is any housing unit of a taxpayer that was owned for less than 365 consecutive days prior to the disposition of the property with several important exemptions. If the disposition occurred due to, or in anticipation of one or more of the following events, then it would not be considered flipped property:

death of a taxpayer or a person related to the taxpayer;

change in the taxpayer’s household in connection with a related person;

breakdown of a marriage or common-law partnership if the partners have been living separate and part for at least 90 days prior to disposition;

a threat to the personal safety of the taxpayer or a related person;

the taxpayer or a related person suffering from a serious illness or disability;

an eligible relocation (as defined in s248(1) of the ITA);

an involuntary termination of employment of the taxpayer or the taxpayer’s spouse or common-law partner;

the insolvency of the taxpayer; or

the destruction or expropriation of the property.

The CRA’s definition of “flipped property” tries to capture the colloquial definition while introducing a level of certainty by creating a strict cut off point (a “bright line”) of 365 days of ownership. While the cut off is somewhat arbitrary, it eliminates a lot of the grey area as the previous requirement was based on intent of the taxpayer.

The CRA also disallows any loss from a flipped property if it falls under this S12 deeming provision for flipped property. Note that if the property is inventory of the taxpayer (ie. in a business that purposely buys and flips property) the loss would not be denied. This new deeming provision is not meant to capture and “punish” a dedicated real estate flipping business as they already treat any profit as business income.

What about the Principal Residence Exemption?

The Principal Residence Exemption will not exempt the gain from a flipped property. Unless the taxpayer is selling due to one of the exemptions, even if the property they sell is their personal residence, the gain will not meet the Principal Residence Exemption because the proceeds are deemed business income due to this new anti-flipping measure. See paragraph 2.6 of Income Tax Folio S1-F3-C2 for a detailed explanation why.

Potential GST/HST Implications

The Excise Tax Act (the “ETA“) imposes an obligation to remit GST/HST on taxpayers who are considered a “builder” under the Act. A taxpayer can be considered a “builder” if they resell a newly constructed property (ie. buying and selling a pre-construction condo soon after closing) or sell a property in which they substantially renovated.

For taxpayers who have deemed flipped property business income and meet the builder definition of the ETA, they will be required to remit to the CRA GST/HST. This means that the transaction price of the property will be deemed to include GST/HST that the seller will need to remit to the CRA which will further erode the profit, if any, from a flipping transaction.

Tips

If a taxpayer is in the situation of selling within the 365 day ownership period due to one of the exemptions, they should retain documentation for proof. The taxpayer has the burden to prove to the CRA that an exemption applies if the taxpayer is audited. Furthermore, the taxpayer should consult with a tax professional to ensure that their situation and/or documentation is sufficient to meet the exemption. By consulting a professional and relying on their expertise, it also offers taxpayer a layer of protection as the taxpayer has done their due diligence.

The CRA implements several algorithmic tools to flag returns for audits. If a taxpayer has a history of claiming the Principal Residence Exemption frequently, it might flag their return for a questionnaire and potentially an audit. Note that the CRA can reassess a taxpayer’s T1 return up to three years after the original Notice of Assessment but if the CRA alleges fraud or misrepresentation, they can reassess further back. In these audits and reassessments the burden of proof is always on the taxpayer therefore it is vitally important to consult a tax professional as early as possible in the process. Whatever the taxpayer tells the CRA should be able to be corroborated or proven through documentation or third parties.

Taxpayers should keep in mind that even if a property is sold after the 365 holding period, the transaction might still be considered business income from a flip. The determination will be based on the facts of the situation.

The anti-flipping measure is coming at a difficult time for taxpayers. With the increase in interest rates and mortgage payments, some home owners may find themselves in a difficult position financially. If the home owner has owned the property for less than 365 days, they might be caught under this anti-flipping measure even if they do not think they are flipping property.

The federal government released the Regulations with more details on exemptions and enforcements on December 21st 2022, this article has been updated to include those new details.

**March 28th 2023 UPDATE**

The regulations were amended on March 27th 2023. The foreign ownership percentage of a corporation or entity was changed from 3% to 10% to be considered a Non-Canadian entity. The exemption for work permit holders was also amended, the exemption now only requires that the work permit has 183 days or more validity as of the date of purchase and they have not purchased more than one residential property. Non-Canadians are also now allowed to purchase residential property if the purpose is for development and can also buy vacant land. The article below will be updated with these changes while noting the old regulations.

Key points of the foreign buyer ban:

It comes into force on January 1st 2023 but will not prohibit any agreements entered into prior to this date.

There are exemptions for some “Non-Canadians”.

Temporary residents who are studying at a designated learning institution and meet all the following: filed all required income tax returns in the five preceding tax years in which the purchase was made, physically present in Canada for a minimum of 244 days in each of the five calendar years preceding the year in which the purchase was made, purchase price does not exceed $500,000, and have not purchased any other residential property in Canada.

Temporary residents who hold a work permit or are otherwise authorized to work in Canada and meet all the following: they have 183 days or more remaining on their work permit on the date of purchase and they have not purchased any other residential property in Canada.*

Foreign nationals who are diplomats, consular staff and members of international organizations.

Temporary residents in Canada due to an exemption under section 25.2 of the Immigration and Refugee Protection Act (IRPA). This is a special exemption for those fleeing international crises (ie. war in Ukraine, Hong Kong residents public policy, etc.) and an immigration professional should be consulted to see if the buyer meets this exemption.

A refugee with a successful claim in accordance with subsection 99(3) or IRPA. Again, please consult with an immigration professional.

The ban only applies for some residential properties.

Does not apply to residential properties outside of census agglomerations or census metropolitan areas. This exemption is meant to exempt certain recreational properties (ie. cottages) that would otherwise be caught in the foreign buyer ban but it should be noted that some cottage areas are not excluded.

Does not apply to residential properties with four or more individual dwelling units (ie. quadplexes and more, or apartment buildings).

There are exemptions for some types of purchases

Acquisition due to death, divorce, separation or a gift.

Rental of a property to a tenant for the purpose of its occupation by the tenant.

Transfer under the terms of a trust that was created prior to January 1st 2023.

Transfer resulting from the exercise of a security interest or secured right by a secured creditor.

Consequences for any person who contravenes the foreign buyer ban is a $10,000 fine.

Furthermore, the non-Canadian can be ordered to sell the property bought in contravention of the ban and the most the non-Canadian purchaser can receive from the sale is the purchase price they paid for the property when they bought it.

The Act comes into force on January 1st 2023 until December 31st 2024 and is meant to be a temporary measure to reduce foreign demand for Canadian real estate to alleviate the housing crisis in Canada.

The foreign buyer ban will not affect foreign buyers who have already entered into a binding agreement of purchase and sale prior to January 1st 2023. The ban also applies to buyers signing pre-construction APSs and assignees during the period of the ban.

Who is banned from buying?

The Act applies to “non-Canadians”. Section 2 of the Act defines “non-Canadian” to mean:

Individuals who are neither Canadian citizens, registered Indian, nor permanent residents of Canada.

Corporations incorporated outside Canada.

Corporations incorporated in Canada but controlled by foreign corporations or individuals who are not Canadian citizens nor permanent residents of Canada. The Regulations have a strict definition of control; direct or indirect ownership of shares representing 10% or more of the value of the equity or voting rights OR control in fact through ownership agreements, etc.

Other persons/entities to be defined in the Regulations.

Importantly, there are several exemptions to the foreign buyer ban outlined in subsection 4(2) of the Act:

Certain students in Canada who meet the following requirements:

Must be studying at a designated learning institution (a list which can be found here). There are some small private colleges that might not be on this list.

Filed all required income taxes in the preceding five years in which the purchase was made. Note that only required income taxes need to be filed, students who had no income or other filing requirements do not need to file those preceding year tax returns.

Physically present in Canada for a minimum of 244 days in each of the five years preceding the date of purchase. This means that the students needs to have been in Canada for at least five years to meet this requirement. The 244 days is meant to cover the typical school term.

The purchase price of the residential property does not exceed $500,000.

They have not purchased more than one residential property. The wording in the Regulations is not very clear but my interpretation is that the purchase must be their first residential property. Property owned outside Canada does not count based on the Regulations.

Certain workers in Canada who meet the following requirements.

Hold a work permit or are otherwise authorized to work in Canada. Some temporary residents in Canada do not need a work permit and they would still be eligible for this exemption.

Have 183 days or more of validity remaining on their work permit or work authorization on the date of purchase. The date of purchase being the closing date on the APS. This requirement was added in the March 27th amendment to the Regulations.

They have not purchased more than one residential property. Again, similar to the student exemption, my interpretation is that the purchase must be their first residential property and property owned outside Canada does not count.

Diplomats, consular staff, and members of international organizations.

Temporary residents in Canada under a visa provided under section 25.2 of the IRPA. This visa is provided for humanitarian and compassionate reasons and meant to exempt those fleeing international crises (ie. war in Ukraine, Hong Kong residents public policy, etc.). This is a very useful exemption as it means the buyer does not need to meet the other requirements for temporary resident students and workers above.

Refugees who have made a claim for refugee protection under subsection 99(3) of the IRPA and the claim has been found eligible.

Non-Canadian individuals who purchase with a spouse who is a Canadian citizen, permanent resident, registered Indian, a refugee, or a temporary resident who meets the student and worker exemptions above.

Types of Property Affected?

The foreign buyer ban applies to “residential property” under the Act, meaning:

Detached houses or similar buildings containing less than four dwelling units.

A part of a building that is intended to be owned apart from any other unit in the building (ie. semi-detached house, rowhouse, condominium unit).

Vacant land that is zoned for residential or mixed use located within a census agglomeration or a census metropolitan area (more on the definitions below).

The Regulations exclude property outside a census agglomeration (CA) or a census metropolitan area (CMA). A CA has a core population of at least 10,000 and a CMA has a total population of at least 100,000 of which 50,000 or more live in the core. This exclusion is meant to exclude recreational properties, mainly cottages, from the ban but some popular areas such as Squamish in BC and Collingwood, Wasaga Beach and Kawartha Lakes in Ontario are included. CA and CMAs can be confirmed here by filtering for CA/CMA.

What are the consequences?

Every person who contravenes OR helps contravene the foreign buyer ban will be guilty of an offence and liable to be fined up to $10,000. Real estate agents, lawyers, builders, and even sellers should be aware of the wide reaching implications of these penalties.

Section 7 of the Act also states that the court may order the property bought under the foreign buyer ban to be sold. The Regulations state that the order for sale can only be made; if the non-Canadian is still the owner when the order is made, notice has been given to every person who may be entitled to receive proceed from the sale, and the impact would not be disproportionate to the nature and gravity of the contravention.

More importantly the order will result in the non-Canadian receiving an amount not greater than the purchase price they paid for the residential property. Meaning that after repaying any court costs and Canadian co-owners or third parties (ie. mortgage, liens, other creditors, etc), any net gain is paid to the government. This is potentially a much bigger “fine” than the $10,000.00 for contravening the foreign buyer ban.

Conclusion

The two year foreign buyer ban along with the recent changes to the GST/HST on Assignments and Ontario’s expansion of the NRST is a continuing trend of government intervention to tackle the housing affordability crisis. Combined with the rising interest rate environment and the potential for a recession in the coming years, there will be a lot of uncertainty.

Notes

*Prior to March 28th 2023, the requirements were: worked full time (30hr/week) in Canada for a minimum three years within the four years preceding the year in which the purchase was made, filed required income tax returns for said years, and have not purchased any other residential property in Canada

The Ontario Non-Resident Speculation Tax (NRST) has gone through several changes throughout 2022. This article will summarize the changes as of the end of 2022 going into 2023.

Summary of NRST changes throughout 2022.

Before March 30th 2022, the tax rate was 15% and it applied to the “Greater Golden Horseshoe” area. NRST rebate available for foreign nationals who become PR within four years, student enrolled for at least two years from the date of purchase, or legal full time working in Ontario for one year from the date of purchase.

From March 30th 2022 to October 25th 2022, the tax rate increased to 20% and it applied province wide. Rebate ONLY available for foreign nationals who become PR within four years.

Since October 25th 2022, the tax rate increased to 25%.

If you want to read the Ontario government’s information on the Non-Resident Speculation Tax, this is their official website.

The NRST applies to foreign entities and taxable trustees that purchase certain types of residential property located in Ontario.

There is a transitional provision that exempts property outside of the Greater Golden Horseshoe if the agreement of purchase and sale was entered into before March 30th 2022.

Foreign entities include individuals who are not Canadian citizens or permanent residents and foreign corporations. Taxable trustees are those who have at least one trustee who is a foreign entity or a beneficiary of the trust is a foreign entity.

Property subject to the NRST

The NRST applies to property that contains at least one, but less than seven, single family residences. Single family residences include detached houses, semi-detached houses, townhouses, and condominium units. This also includes duplexes, triplexes, fourplexes, fiveplexes, and sixplexes.

Therefore, buildings that contain seven or more single family residences (ie. rental apartments), commercial, vacant, and industrial land are excluded from the tax.

How the NRST is calculated and paid

The NRST rate is 25% of the value of the consideration for the residential property. In most cases, this will be the agreed upon sale price on the APS.

Again, transitional provisions apply to if the APS was entered into prior to the dates outlined above.

The NRST also applies to 100% of the value of the consideration even if the foreign entity only owns a portion of the property being purchased. Each purchaser is jointly and severally liable for any NRST payable.

The NRST will be paid as part of the lawyer closing process. The transferee will need to provide the lawyer with the NRST amount with the down payment of the property.

NRST Exemptions

The following NRST exemptions apply and they have not changed throughout 2022:

If the foreign national is a nominee of the Ontario Immigrant Nominee Program at the time of purchase and the property is used as the foreign national’s principal residence.

If the foreign national is a convention refugee under IRPA at the time of of purchase.

If the foreign national is jointly purchasing with a spouse who is a Canadian citizen, permanent resident, Ontario Immigrant Nominee Program nominee, or refugee.

NRST Rebates

If a foreign national bought a property after March 29th, 2022, the only rebate available is if the foreign national becomes a Canadian permanent resident within four years of the date of purchase. The date of purchase meaning the closing date of the property transaction when the transfer/deed is registered by the lawyer.

The requirements of the permanent resident rebate are as follows:

the foreign national must become a Canadian permanent resident within four years of the date of purchase,

the property must be owned only by the foreign national or by the foreign national with their spouse,

the property must be used as the foreign national’s principal residence for the entire period, and

the rebate application must be received by the Ontario Ministry of Finance within 90 days of the foreign national becoming a permanent resident of Canada.

NRST Rebate transitional provisions

Transitional provisions apply for the student and worker rebates if the APS was entered into prior to March 29th 2022 but the complete application must be submitted by the earlier of:

four years after the date of purchase, or

March 31st, 2025.

NRST Rebate Application Procedure

When we apply for the NRST rebate, we usually include it with any Land Transfer Tax (LTT) rebate for first time home buyers if applicable (see below for more details on timeline).

A complete rebate application should have the following:

Ontario Land Transfer Tax Refund/Rebate Affidavit

Registered transfer

APS, and/or assignment documents with all schedules attached.

Statement of Adjustment

Proof of payment of the LTT and NRST

Proof of occupancy as principal residence with 60 days of closing

Proof of status as permanent resident (or fulfilment of study or work requirements if applying for the transitional rebates)

In most cases, the applicant should have most of the documents required to submit the rebate application but if not, they should follow up with the lawyer they used for closing who will have the Transfer, statement of adjustment, Teraview docket summary, etc. Note that most lawyers will charge an additional legal for the rebate application process because it is not included in their original retainer.

Proof of occupancy could include utility, phone, credit card statements, delivery slips, moving invoice, etc. that support the use of the property as the foreign nationals principal residence throughout the ownership period. The government gives a grace period of 60 days but it is expected that the applicant must be able to prove they moved into the property within this time.

Proof of status for permanent resident status would be a PR card or the Confirmation of PR document.

For the transitional rebate provisions for students, a study permit, an official transcript showing full time study for two years after the date of purchase and invoices to show tuition payments is generally sufficient. A school letter confirming enrollment would also be advisable in some situations.

For the transitional rebate provision for workers, work permit, T4s, pay stubs, and an employer letter confirming employment is generally sufficient.

Other Considerations

If the foreign national is also a first-time home buyer, they may be eligible for the LTT rebate from Ontario and/or Toronto if applicable. The rebate only applies if the foreign national becomes a permanent resident and the deadline for application is more strict than the NRST. The deadline to apply for the LTT rebate for first time home buyers is within 18 months of the date of purchase.

It is very important to make sure these rebate applications are complete because processing time can take almost a full year. If an incomplete application is submitted, it could take months before the problem is detected and by that time, the time limits above could be exceeded. If you need help, please reach out to us.

To stay up to date on any future changes to the NRST or to stay up to date on global mobility issues, sign up to our newsletter using the form below.

The 2022 Federal budget included a few changes to the way some real estate transactions are taxed. The two mains changes are the new residential property flipping rule and changes to the way GST/HST on assignments is taxed for individual. In this post I will be discussing the latter.

Summary of the changes to GST/HST on assignments effective May 7th 2022:

The new change makes it so that there is GST/HST on assignments regardless of original intentions. Previously, if the original intention of entering the pre-construction contract/Agreement of Purchase and Sale (APS) was for personal use, GST/HST on assignments did not apply. But if the intention was to sell for profit or flip the property, GST/HST applied.

The legislation officially recognizes that GST/HST is not payable on the portion of the consideration exchanged that represents the deposit that the assignor paid to the seller/builder.

I have seen people talk about these changes as if it will slow down the housing market because they seem to incorrectly assume that GST/HST on assignments is double levied or increased. The changes actually add certainty to the way GST/HST on assignments are taxed.

Let’s do an example of pre- and post- May 7th 2022 changes. Here is the assignment details (closely maps on to OREA Form 145/150 Schedule B):

Purchase Price on the original APS = $1,000,000

Payment by Assignee to Assignor for this Assignment Agreement = $100,000*

Total Purchase Price including the Original APS and this Assignment Agreement: $1,100,000

Deposit paid by the Assignor to the seller under the original APS to be paid by the Assignee to the Assignor: $200,000

**For the sake of simplicity, this excludes GST/HST but in practice, most assignment agreements will stipulate that GST/HST is included

Under the pre-May 7th 2022 rules according to the CRA*, GST/HST would have been payable on the whole amount that the assignee pays to the assignor, $300,000, which results in HST payable of $39,000 in Ontario (13%*300,000).

*Note that it was the CRA’s view that GST/HST is levied on the deposit. In reality this was challenged successfully in a 2013 Tax Court case and a taxpayer can file their GST/HST return without including the amount attributable to the deposit. But the CRA continued to levy GST/HST on the deposit amount in audits and reassessments so taxpayers unaware of the Tax Court ruling would end up paying additional GST/HST.

Under the post-May 7th 2022 rules, GST/HST on assignments is officially only payable on the payment by the assignee to the assignor, $100,000, which results in HST payable of $13,000 in Ontario. This will force the CRA to update their practice guidelines and hopefully they will no longer expect GST/HST on deposits in audits and reassessments.

The Nitty-Gritty

Lately, I have seen a lot of incorrect information shared by investors, agents, accountants, and lawyers regarding the new GST/HST changes so I hope that this post can put to rest any uncertainty on this issue by giving concrete examples and referring to the budget documents (the link goes to the Supplementary Information attached to the Federal Budget).

Many people are confused about the new changes to GST/HST on assignments and I think it largely stems from the imprecise use of language when talking about assignment agreements.

Before we begin, let’s start with some general definitions I will use in this post and are relevant in assignments:

APS = Agreement of Purchase of Sale = Pre-Construction Contract

Buyer = Assignor. The buyer is the individual who signed APS to buy the property. They will also be the assignor in the assignment agreement by assigning the APS to the assignee.

Seller = Builder. The seller is the builder who signed the APS to sell the property. Note that most pre-construction agreements have a clause that give the seller some rights in an assignment of the contract (ie. seek seller permission and/or an assignment fee).

Assignee = first occupant. The assignee is the person who will be assigned the APS and wants to eventually close on the property and live in it therefore, in most cases, they will be the first occupant.

Taxable Supply – means a supply that is made in the course of a commercial activity (from the Excise Tax Act (the “ETA“) S123(1))

Budget Day – April 7th 2022.

There are two main paragraphs most relevant to the new changes and I will explain what both of them mean. The first:

Budget 2022 proposes to amend the Excise Tax Act to make all assignment sales in respect of newly constructed or substantially renovated residential housing taxable for GST/HST purposes. As a result, the GST/HST would apply to the total amount paid for a new home by its first occupant and there would be greater certainty regarding the GST/HST treatment of assignment sales.

Supplementary Information for the 2022 Federal Budget (https://budget.gc.ca/2022/report-rapport/tm-mf-en.html#a5_2)

I believe some people have misinterpreted this paragraph, specifically the underlined section. The total amount paid by the first occupant is the purchase price on the APS (net of GST/HST as it is usually included in the price) plus the amount the first occupant/assignee paid for the assignment contract (also net of GST/HST).

The legislators have reframed the GST/HST on assignment sales from a taxable supply provided by the assignor, to the GST/HST owed because that is the “true purchase price” that the first occupant paid for the property. There is no double taxation. The amount of GST/HST on assignments is just being levied on the original APS price plus the additional amount the assignee paid to the assignor.

Which leads to the next paragraph:

Typically, the consideration for an assignment sale includes an amount attributable to a deposit that had previously been paid to the builder by the assignor. Since the deposit would already be subject to GST/HST when applied by the builder to the purchase price on closing, Budget 2022 proposes that the amount attributable to the deposit be excluded from the consideration for a taxable assignment sale.

Supplementary Information for the 2022 Federal Budget (https://budget.gc.ca/2022/report-rapport/tm-mf-en.html#a5_2)

The GST/HST on the deposit never made sense because the assignee was essentially returning the deposit that the assignor already paid to the builder which was already subject to GST/HST in the APS. This new reframing of the assignment sale solves that quirk because the deposit is already accounted for in the assignee’s “true purchase price”.

The Nittier-Grittier

So this is where going to law school comes in handy. If the above has not convinced you, please read on but otherwise, this might be a bit dense as I convert each part of the change to the ETA in everyday language that even a non-tax lawyer can understand (hopefully).

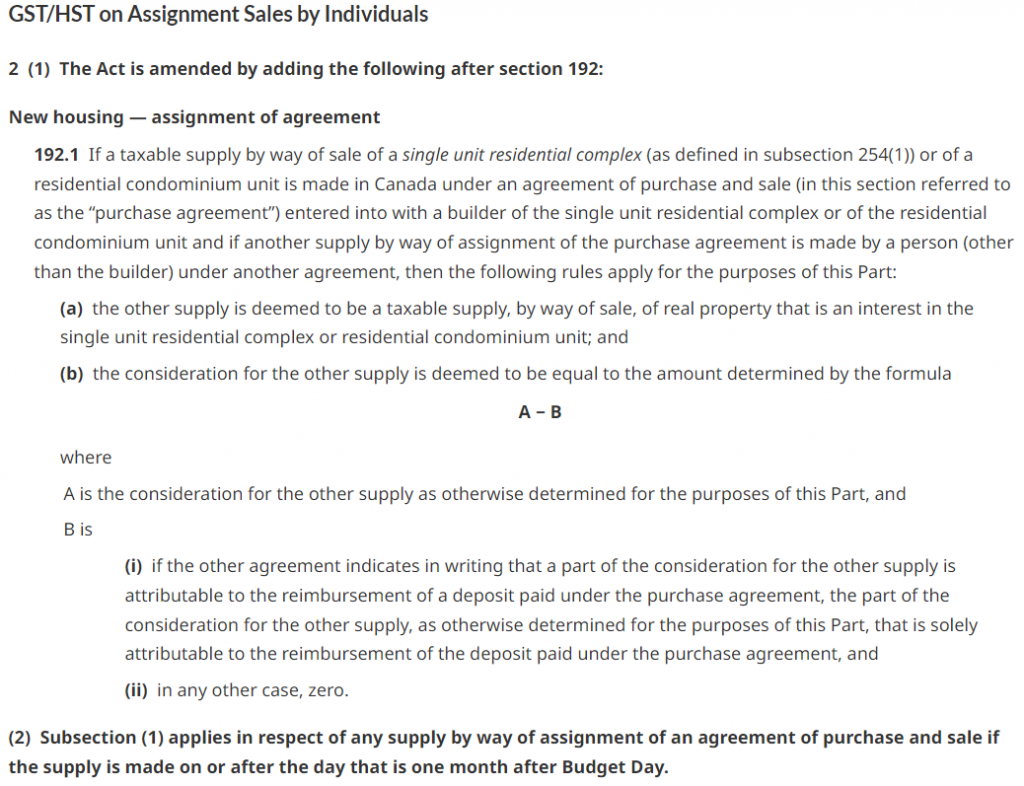

Supplementary Information for the 2022 Budget (https://budget.gc.ca/2022/report-rapport/nwmm-amvm-02-en.html)

If a taxable supply by way of sale of a single unit residential complex (as defined in subsection 254(1)) or of a residential condominium unit is made in Canada under an agreement of purchase and sale (in this section referred to as the “purchase agreement”) entered into with a builder of the single unit residential complex or of the residential condominium unit […]

Translation/simplification: If a taxable supply by way of an APS is entered into …

[…]and if another supply by way of assignment of the purchase agreement is made by a person (other than the builder) under another agreement, then the following rules apply for the purposes of this Part:

Translation/simplification: …and if there is another supply (profit from the assignment) by way of the assignment of the APS, then the following rules apply:

(a) the other supply is deemed to be a taxable supply, by way of sale, of real property that is an interest in the single unit residential complex or residential condominium unit; and

They key phrase here is “other supply” because it does not refer to the original taxable supply which would have been the entire purchase price of the property in the APS. Instead, the “other supply” refers to the profit the assignor made in assigning the APS to the assignee.

Translation/simplification: (a) the profit from the assignment agreement is deemed to be a taxable supply.

(b) the consideration for the other supply is deemed to be equal to the amount determined by the formula A-B where

Translation/simplification: (b) the profit from the assignment agreement is determined by the following formula A-B where

A is the consideration for the other supply as otherwise determined for the purposes of this Part, and

Translation/simplification: A is the total amount the assignor received before HST, and

B is

(i) if the other agreement indicates in writing that a part of the consideration for the other supply is attributable to the reimbursement of a deposit paid under the purchase agreement, the part of the consideration for the other supply, as otherwise determined for the purposes of this Part, that is solely attributable to the reimbursement of the deposit paid under the purchase agreement, and

(ii) in any other case, zero.

Translation/simplification: B is a reimbursement from the assignee to the assignor for the deposit paid in the APS if applicable

And putting it all together:

If a taxable supply by way of an APS is entered into and if there is another supply (profit from the assignment) by way of the assignment of the APS, then the following rules apply

(a) the profit from the assignment agreement is deemed to be a taxable supply.

(b) the profit from the assignment agreement is determined by the following formula A-B where

A is the total amount the assignor received before HST, and

B is a reimbursement from the assignee to the assignor for the deposit paid in the preconstruction agreement if applicable

Conclusion

This new change introduces more certainty and logic into the tax code which is good for society overall.

Realistically, this only disadvantages those who have a change in circumstance and are “forced” to assign their property before closing. For example, this could be due to interest rate hikes that prevent a taxpayer from obtaining a mortgage or getting a new job elsewhere and no longer needing the property.

But it does create a positive incentive for real estate flippers to follow the law as it closes off one of the avenues for avoiding GST/HST on assignments (though income tax is a whole other issue). I don’t think it will have any meaningful effect on house prices, unless people believe in the incorrect information.

Bare Trusts are an important tax and estate planning tool that can be used in many contexts. A common example where bare trusts would be useful is in real estate transactions where a parent is on title with the child for mortgage reasons but the intention is for the child to have full ownership of the property.

In law, there are two types of ownership of property. There is the “legal ownership” or “legal title” of the property which is generally held by the person whose name is registered with that property. The second type of ownership is “beneficial ownership”. The beneficial owner is the person who is entitled to the benefits (ie. capital, income, use) of the property.

In most cases, the legal and beneficial owner is the same person (ie. I own a bank account or house for my own uses). But there can be situations where legal and beneficial ownership are split whether intentionally or unintentionally (ie. my name is on the title of a house with my child but my child pays the mortgage and uses it exclusively).

To summarize, a bare trust involves three parties:

The settlor(s) in a bare trust is the beneficiary(s). In other trusts, these parties are often separate.

The trustee(s) who hold legal ownership. In a bare trust (unlike other trusts), the trustee has no independent power, or responsibility for dealing with the trust property. Their only role is to hold legal title.

The beneficiary(s) who hold beneficial ownership. In a bare trust, the beneficiary has the right to the capital, assets, and income of the trust property. The beneficiary is also the person who will be the decision maker for dealing with the trust property.

A bare trust agreement drafted by a lawyer is important because it establishes a legitimate bare trust relationship between the parties. If there is a future dispute as to whether a bare trust exists between the parties, the trust agreement would be the primary proof that such a relationship exists. A properly executed trust document is the best defense to the CRA or other parties alleging an alternative arrangement.

Some potential issues to think about:

A trustee in a bare trust has very limited responsibilities with respect to the trust property, but this is not necessarily true in other trust relationships. A bare trust agreement will establish the responsibilities of all parties and limit the liability of the trustee while also protecting the beneficiaries rights.

There are a variety of uses for bare trusts in real estate transactions: minimizing land transfer taxes, joint ventures and partnerships, estate planning, etc.

On February 4th 2022, there is draft legislation that proposes new tax reporting requirements for bare trusts. The legislation is not finalized so exact reporting requirements are not known at the moment (written April 27th 2022). If there are reporting requirements, bare trusts could result in some additional tax filing obligations and expenses.

There will be a transitional period for Agreements of Purchase and Sale entered before March 30th 2022. The previous Non-Resident Speculation Tax (NRST) rate of 15% for the Golden Horseshoe Region applies for any APS entered prior to the aforementioned date. The new NRST changes were implemented by the Ontario government to reduce foreign demand for Ontario housing in the hopes of slowing down the housing market.

Any foreign national (individuals who are not Canadian citizens or permanent residents of Canada) who purchases property in Ontario will be subject to the 20% NRST from March 30th onward.

Furthermore, the NRST rebate for International Students and Foreign Nationals Working in Ontario no longer applies from March 30th 2022 onwards. If you were relying on this rebate and the agreement was entered into prior to March 30th, you can still claim the rebate but the application must be submitted before March 31st 2025.

If you are still eligible to claim an NRST rebate under the old rules before the new NRST changes, please contact us. We help people apply for rebates of both the NRST and LTT (Ontario and Toronto). As of November 2022, these rebate applications are taking almost one year to process from the time of submitting the documentation. It is vitally important to provide the appropriate evidence necessary for the application to avoid further delay or rejection especially as there is now a new deadline for applying for such rebates; March 31st 2025.

When you have a change in use of a property from being your principal residence to a rental property or vice versa, s45(1) of the Income Tax Act deems that a disposition of the property has occurred. For more information, please see our post regarding the principal residence exemption.

A s45(2) election may be applicable when the change in use is from your principal residence to a rental property. S45(2) postpones the change of use deemed disposition and allows you to maintain the principal residence designation on your home for up to four years after you have stopped living in it. This post will discuss the requirements for the election to be valid and the resulting tax implications.

I will also go over the s45(3) election used when you have a change in use from an income property to your principal residence at the end of this post.

Who can make a s45(2) election?

You must not designate any other property as your principal residence and you must be a resident or deemed to be a resident of Canada. Residency determination of a taxpayer is another big topic for another post. But you do not have to be a permanent resident or citizen of Canada to be resident of Canada. The determination is based on the facts of circumstances of each case.

When to make a s45(2) election?

The s45(2) election should be made during the taxation year in which the change in use occurred. Intuitively, this makes sense, if the s45(2) election was not made you would have to report a disposition of your principal residence on your tax filing for the year.

The CRA allows you to file a late s45(2) election but you may be subject to penalties. Furthermore, you cannot claim Capital Cost Allowance during the period when the property was used for income purposes that you want to claim principal residence exemption on. You should contact us if you plan to make a late election, there could be penalties if the request is seen as retroactive tax planning, there is inadequate documentation, or you are considered negligent in complying with the law.

Tax implications of a s45(2) election

Since you are only allowed to designate one principal residence per family unit, if you decide to make an s45(2) election, you will not be able to designate any other property during that period as your principal residence. Careful consideration should be put into the current and future valuation of the property subject to the election and any other property you own.

Extension of a s45(2) election

The standard s45(2) election allows the principal residence exemption to cover four additional years where you do not live in the property. If the following conditions are met, the four year limit can be extended indefinitely:

You moved because you or your spouse/common-law partner’s employer wants you to relocate.

You are your spouse/common-law partner are not related to the employer.

You return to your original home while you or your spouse/common-law partner are still with the same employer, OR before the end of the year following the year in which this employment ends, OR you die during the term of employment.

Your original home is at least 40km farther than your temporary residence from you or your spouse/common-law partner’s new place of employment.

You should be retaining and collecting documentation in support of any of the above conditions in case the CRA audits your election. If you are audited for such an election please contact us as these disputes are very fact specific.

Section 45(3) Election

A s45(3) election may be beneficial when the change in use is from an income producing property (rental property) to your principal residence. A successful election will allow you to declare a property your principal residence for up to 4 years before the change in use occurs.

For example, say you have a rental property that has been rented for 5 years that you moved back into as your principal residence for 2 more years before finally selling it. A s45(3) election will allow you to declare the subject property your principal residence for 6 years instead of just 2 years if the election was never made. This could be a huge tax saving.

Furthermore, an s45(3) election eliminates the deemed disposition that would otherwise be required by the CRA in a change in use scenario. You still need to consider the value of the property at the time of the change in use (and expected change in value in the future) to determine whether a s45(3) election is worth it in your scenario. In some scenarios, an s45(3) election might result in a much higher tax burden therefore a careful calculation with an accountant or tax planning lawyer should be conducted.

Similar to the s45(2) election, the s45(3) election is only available if CCA was not claimed on the property. And again, if you have more than one property, you should consider whether the principal residence exemption is more valuable on one property over another.

Unlike the s45(2) election, the s45(3) election is made in the tax year in which the property is actually disposed of, NOT the year in which the change in use occurs.

Conclusion

S45(1) change in use dispositions can seem like a headache but the elections covered above offer some substantial tax savings and tax planning opportunities. This article only covers the main considerations in such an election. To properly consider whether you should make an election we need to calculate the tax savings, consider opportunity costs, tax residency, and a variety of other legal matters. If you are considering such an election or have further questions, please contact us!

A house is often a person’s most valuable asset, making the principal residence exemption the biggest tax break most people can get. What most people are not clear about is when your house can be considered your principal residence. For example:

If I rented out a part of my house, can I still claim a principal residence exemption? (yes, but it depends)

I started renting out my house and no longer live there, does that mean I have made a deemed disposition of my principal residence? (no, but it depends)

If I only lived in the house for a few days in a year, can it still be considered my principal residence? (yes, but it depends)

They key is always in the details and hopefully this post will shed some light on when the principal residence exemption is actually applicable.

First of all, all this information is freely available in the CRA’s Income Tax Folio S1-F3-C2 on the topic of principal residence. Be forewarned that it is a length webpage but it is thorough and may cover specific situations not covered in this post. It should be noted that from a legal perspective, the CRA Income Tax Folio’s are only the CRA’s interpretation of the Income Tax Act. When we create a tax plan or represent you in a tax dispute, we also rely on case law and other legal arguments which produce a more favourable interpretation of the Income Tax Act specific to your situation. If you have a specific situation in mind please contact us.

With that being said, let’s go over some topics that frequently come up when we talk about the principal residence exemption.

The principal residence exemption only exempts capital gains

You should keep in mind that if the CRA claims that the sale of your property resulted in business income and not capital gains, then the principal residence exemption will not apply whether you lived in the property or not. This is because a precondition for the exemption is that the income must be a capital gain.

The CRA may reassess a sale as business income based on several factors which they use to imply a house flipping transaction. Not only would you lose the exemption, but 100% of the profit will be taxes based on your marginal tax rate and you will liable to pay HST/GST with interest.

Ownership considerations

To claim the principal residence exemption on the sale of a property you must own the property. This might seem obvious but there are several further implications.

In a situation where the title of the property is held as joint tenants between several people; upon the sale of the property, the capital gain will generally be split between the parties equally. The principal residence exemption will only be available to the taxpayer who can meet the requirements to designate the property as their principal residence. The same applies for property owned as tenants-in-common subject to whatever percentage ownership on title.*

Who can use the principal residence exemption?

You can only designate one principal residence for a particular tax year for your family unit. Note that it is family unit and not individual, this has both advantages and disadvantages. Advantage, you can designate a property you do not live in, but a member of your family unit lives in, as your principal residence. Disadvantage, you cannot designate multiple principal residences among your family unit.

A family unit consists of:

You

Your spouse or common-law partner throughout the year, unless the spouse or common-law partner was living part due to a judicial separation or separation agreement.

Your child, except those who are married, in a common-law partnership, or 18 years or older.

If you are 17 years or younger and are not married or in a common-law partnership: your parents and siblings who are not married, in a common-law relationship, or 18 years or older.

The ordinarily inhabited rule

This is usually where people get confused because there is a lot of grey area in determining whether a property is ordinarily inhabited by a member of your family unit. There is the obvious situations, where you live at the property throughout the ownership period. But depending on the circumstances, the exemption could also be applicable if your child intended to live in the property but never got the chance. It comes down to the reason you owned the property in the taxation year you are claiming the exemption. But since people very rarely write down the exact reason we do certain things, we can usually only offer circumstantial evidence that hints at the reason. This is why record-keeping for these tricky situations is so important and why a dispute with the CRA requires very careful and structured arguments.

Generally speaking, if the evidence shows that the main reason you owned a property is for profit or income production, then it will generally not be considered ordinarily inhabited; the capital gain attributed to that year may not be exempted by the principal residence exemption. Or if the evidence suggests that the property was acquired with the intention of flipping for a profit, the entire gain may be considered business income.

What if I rented out only a part of my home?

This is another grey area. The general rule is that if you are renting out a part of your principal residence, then that portion of the property is not covered by the exemption. For example, this would apply if you had a commercial store front as part of the property.

There is an exception for people who rent out their basement or a bedroom in their house. If the following conditions are met, the principal residence exemption will apply to the entire property:

The income-producing use is ancillary to the main use of the property as a residence.

There is no structural change to the property to make it more suitable for rental purposes.

No Capital Cost Allowance is claimed on the property.

Change in use

When you go from living in your property to renting it out, there is a change in use. For tax purposes under s45(1) of the Income Tax Act, you are deemed to have disposed of it at fair market value and reacquired it at the same price. This deemed disposition updates your adjusted cost base for calculation future capital gains which will not be shielded by the principal residence exemption. You are required to report this change oinuse in the tax filing of the year of the change.

There are two ways to postpone the deemed change of use from principal residence to income property:

A s45(2) election which allows you to keep the principal residence declaration on the property even after you move out for up to four years, and

S54.1 also allows the principal residence exemption if you move due to requirements to relocate due to employment.

Both of these are extremely valuable in tax planning but there are specific requirements and there may be adverse tax consequences. The links above will go to a post with more details.

You can also postpone a change of use deemed disposition when going from an income property to your principal residence with a s45(3) election. In this situation, the property may be designated as the principal residence for a period of up to four years before the change of use. This election too has its own set of requirements.

If you have any further questions, please contact us.

Information current as of December 4th 2020.

* Off-topic but I think it bears mentioning. This is an especially important consideration in an estate plan. In an attempt to avoid probate fees, some people might want to include a child on title of their principal residence as a joint tenant. But if this occurs, the transferring parent will be deemed to have disposed of half their interest in the property and any gain on the half owned by the child will no longer be subject to the principal residence exemption if the property is not the child’s principal residence. The taxable portion of the capital gain could be significantly more than any probate fees saved.